Money moves

Objective-driven, user-centred, iterative design of an intuitive business banking feature

lead product designer

Jun-Jul 2023

figma

Context, Problem & Objective

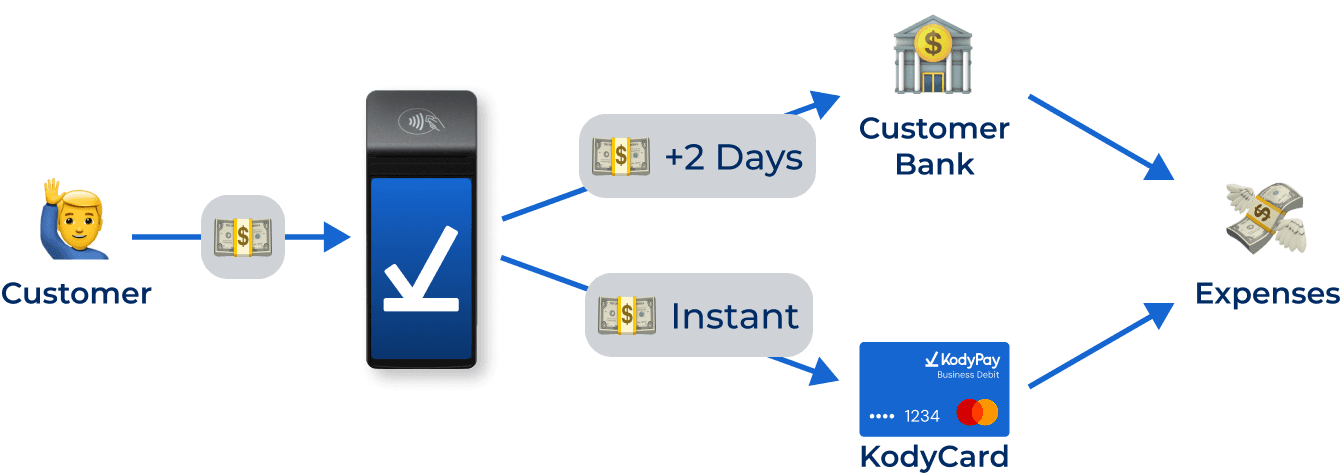

Context: Kody as a payments facilitator

The traditional Payfac funds flow:

Delayed payout

High interchange and banking fees

Cumbersome accounting processes

Limited value-add for Kody

“KodyCards” for business expenses

Business debit cards issued with our partner acquirer bank

Instant access to takings, easy to spend on business expenses

What’s the problem?

Some merchants love having instant access to their funds.

But less than 10% of merchants are actively using the cards pay for expenses.

Even amongst merchants who are using the cards, they are spending a small percentage of their total processed volume.

Problem Statement

Very few merchants have adopted our recently launched card solution. Most still receive their payouts directly to their accounts. This is a problem because the funds are delayed, the interchange fees are high and the accounting is decentralized. It’s also a problem for Kody’s positioning relative to competitors who offer alternatives.

Objectives

What’s our main user-centred objective, and what are the business objectives?

Reduce costs and streamline funds flow for merchants

Generate revenue and build brand value for Kody

Success Metrics

We want to increase adoption and total volume of funds spent using Kody.

5x

merchants spending funds within Kody ecosystem

30%

increase in funds spent using Kody payment methods

Discovery, Research & Definition

How Might We

Optimize our funds flow ecosystem to retain a higher percentage of funds within the Kody platform, thereby enhancing merchant loyalty, increasing revenue, and delivering a seamless and cost-effective solution?

In-depth Interviews

As always, our process started with our users. How do they currently manage their funds? What’s the problem with our debit card? Why aren’t they using it for all expenses?

The Main Pains

Transfers

For most of our merchants, it turns out that the majority of their spending behaviour is through bank transfers, not card payments.

Access

Until now, all of our KodyWallet features have only been available on web - some users are most comfortable banking on mobile.

Expenses

Several merchants are using platforms like Pleo to empower their staff to handle payments, these expense platforms are mature and feature rich.

Spending Types

We estimated that for most merchants this accounted for upwards of 60-80% of their monthly spending.

Popular for high-value, regular payments like rent or utilities. High value, low frequency.

A much smaller portion of monthly expenses (less than 5%) crossed borders, although this is likely to grow as we scale and internationalize

Accounting for a much lower percentage of overall expenses in this particular industry, incumbents offer very attractive reward programs.

Competitor Analysis

Business banks

The majority of our merchants banked with either Revolut, Wise, HSBC or NatWest with a smaller portion banking with Lloyd’s, Santander and Barclays.

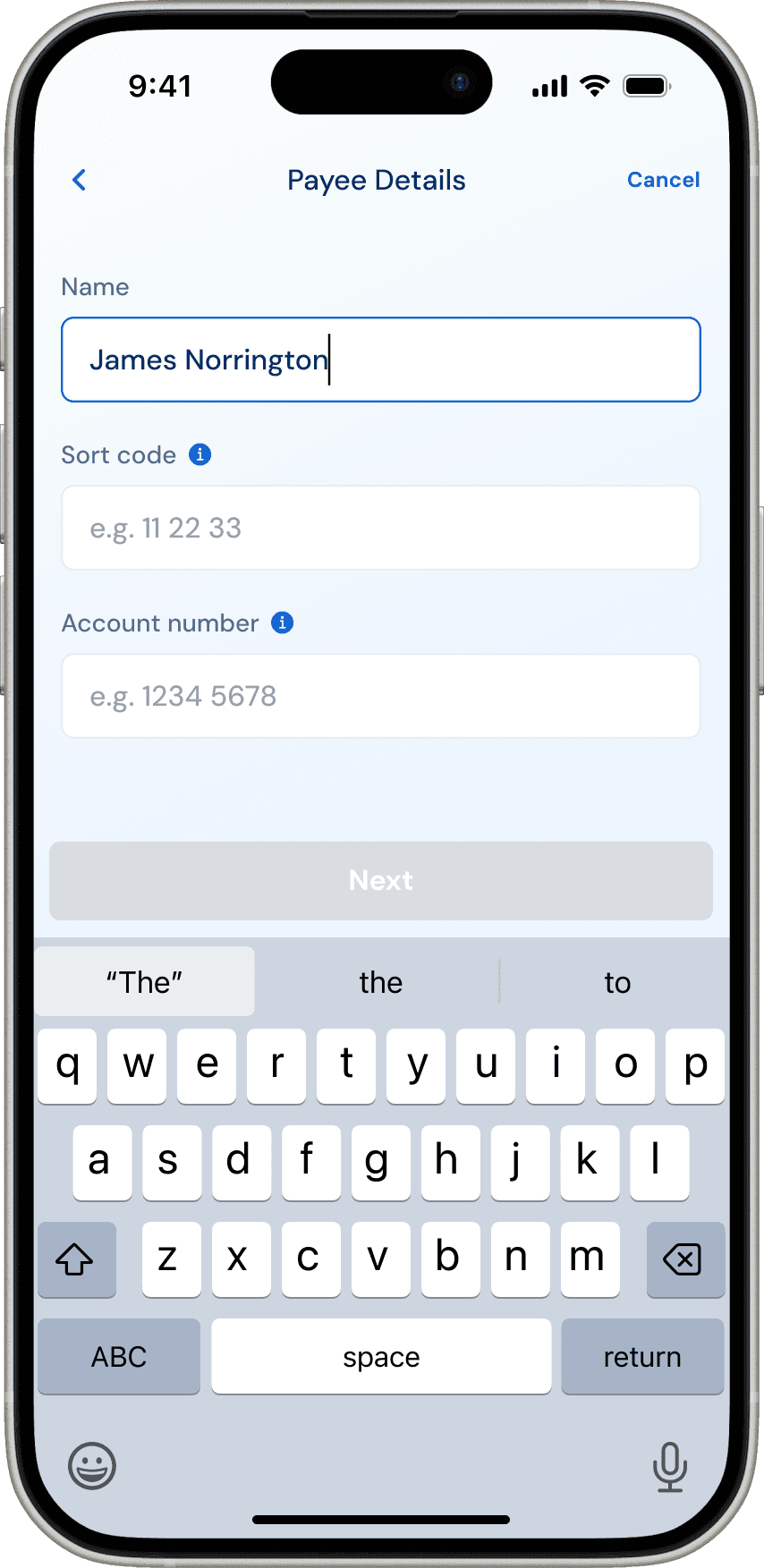

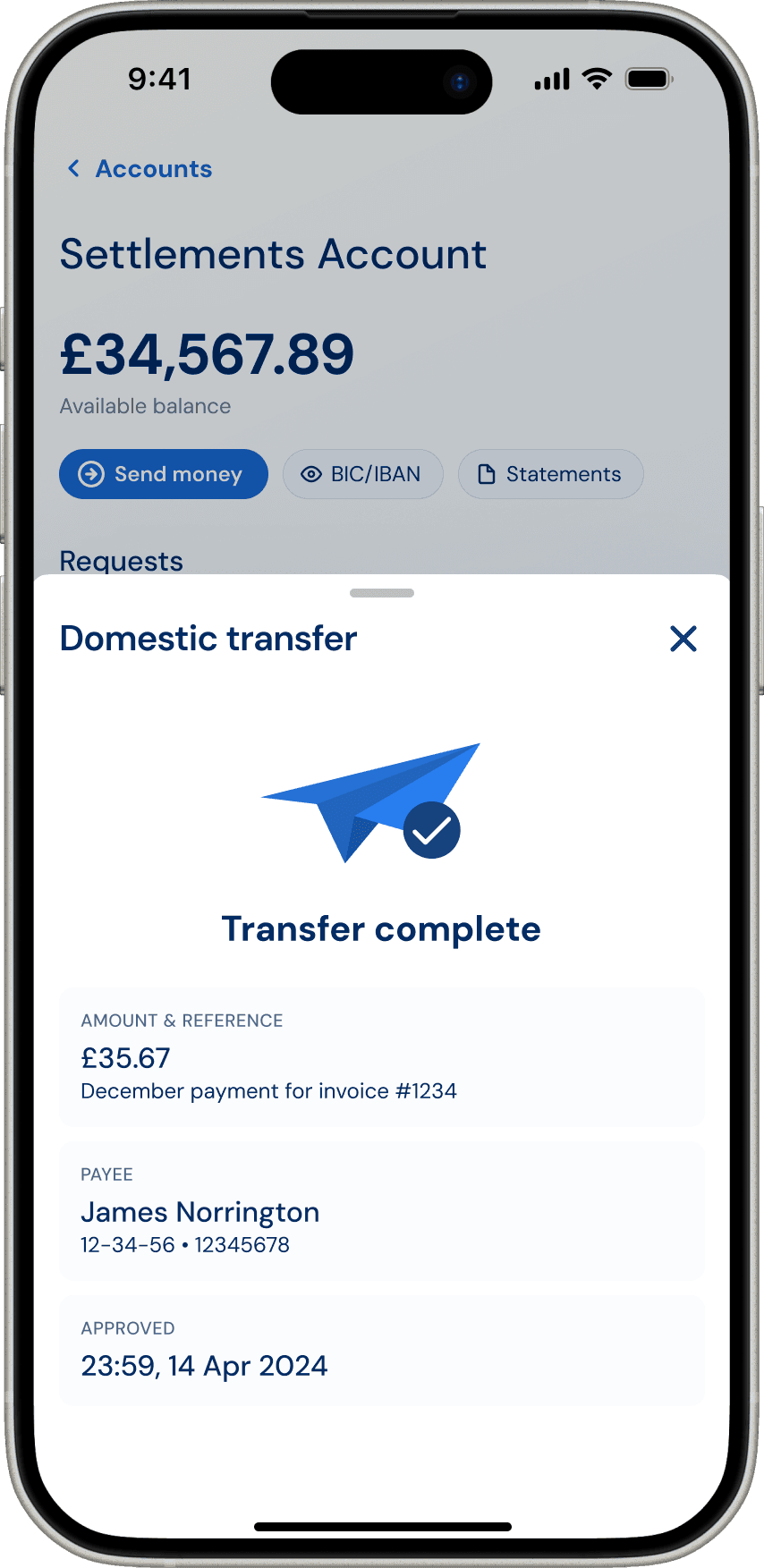

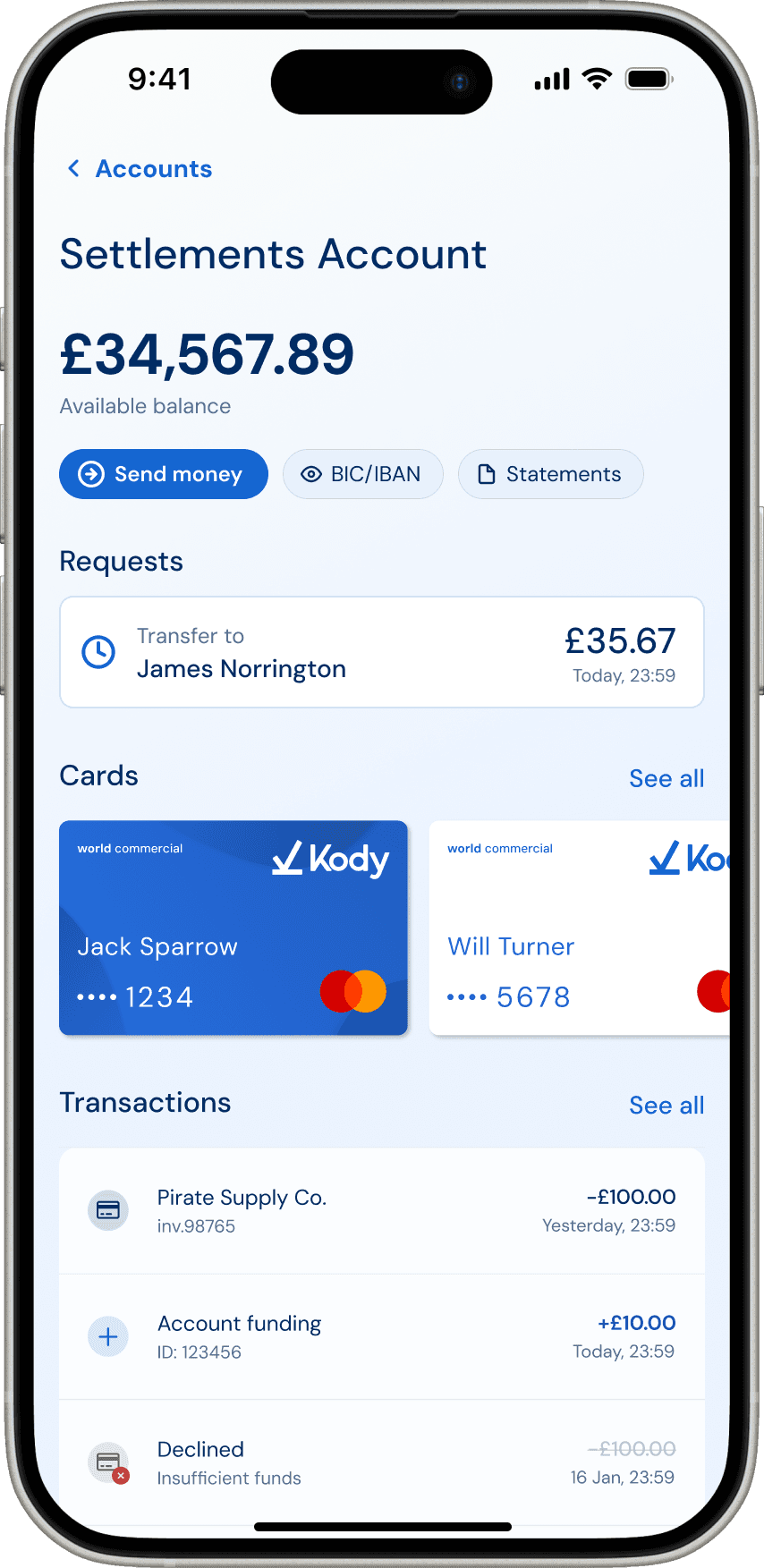

Domestic transfer features

User authentication for safe and secure payments

Sending funds between accounts using sort code and account number (SCAN)

Verifying payees using their personal or business name against the SCAN

Saving payees to easily pay again

Management capacity to review and approve or reject requests

Ability to schedule future transfers and create repeating/recurring transfer events

Technical and compliance constraints

APIs, backend not ready yet

Transfer instrument not yet available. We knew that this type of transfer wasn’t yet supported through our partner institution, but were fairly confident it would be within 4 weeks.

Payee verification APIs unavailable. This work would begin once the transfer instrument was available, so this function can’t be a part of the first release without some delay.

Limited engineers and developers In many cases, the team would be limited to 1 or 2 front-end or back-end engineers at a time, so things like setting up a system for payee management and a system for scheduling transfers couldn’t be developed in parallel and would have to be worked on in sequence.

Domestic transfers require SCA Due to some other technical limitations, we could only offer strong customer authentication through our mobile app

Design & Delivery: Diagrams to Impact

Task flow diagramming

Consensus: an approved MVP

Considering all of our currently known technical constraints and taking into consideration the leaders of the industry and their standard workflows, we considered several options and landed on a simplified transfer flow.

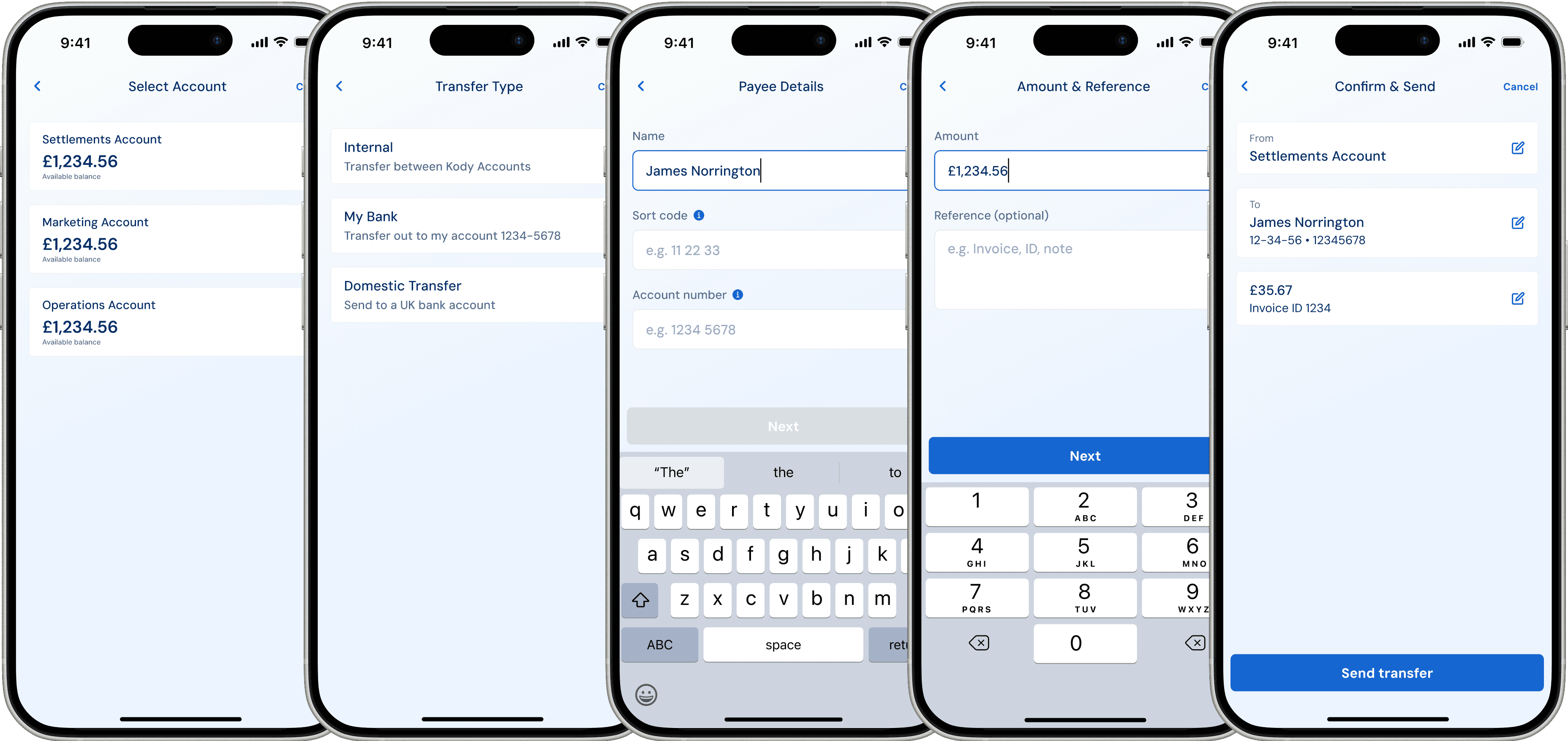

Low-fidelity wireframes

Hi-fi MVP

Beta Launch

Wins

Approximately 20% of our merchant-base signed up for the beta, including some that had not adopted any KodyWallet/Issuing features yet

Learnings

Payee verification is more necessary than previously thought: We underestimated the risk of making mistakes with payee information, resulting in several failed transfers.

“Transfer type” step is confusing: Anecdotal feedback from several merchants, plus unnecessary backtracking in user testing indicate that the three types of transfers confusing - want to try to combine the transfer types with the payee if it’s intuitive.

Approvals deprioritized: We found that most merchants had only enrolled one super-users anyways, making it much less useful to develop the approvals feature next - we decided to focus in on payee management instead.

V2 - Payee Verification

Fast-follow Improvement: Reducing Errors

Wins

Zero failed transfers due to incorrect payee details, saving preferred payees saves time when making transfers, say merchants.

Learnings

Despite an additional step for verifying payees, the time to complete and percentage of error-free transfer attempts seem both to have improved.

Now that it’s been proven to work smoothly, manager/owner users are getting more and more interested in providing staff with access to transfers.

V3 - Transfer Approval

Continuous Improvement: Controlling Spend

Wins

Several active stores created new users in the week following this release, coinciding with an increase in overall spend through the transfer feature.

Learnings

Transfers don’t expire, but there have been instances of transfers not being approved resulting in late payments. Ensuring that managers know they need to approve a transfer is crucial.

Impact & Conclusions

Knowing that this product launch was incremental one of the main success metrics was seeing growth after each iteration. Every deployment could be associated with increases in users and gross transactional volume.

Merchants who were already using KodyCard, on average, increase from under 10% to over 40% of all revenue volume, in some cases, passing through Kody payment instruments, rather than being paid out to merchant bank account.

We increased from approx. 10 active merchants to approx. 25 regularly active merchants, however average number of users increased from 1.5/store to 4/store.

Next steps

Scheduled and recurring transfers

The ability to set a transfer to occur at a future date, and to set transfer events which repeat at some regular interval is the next feature to be added to our business banking app.

Reading statements and predicting transfer events

We’re actively investigating an opportunity to leverage an AI service to scan new merchants existing bank statements to suggest payees and recurring transfers.